![]()

With trusts that their season in hellfire could be moving toward an end, airline stocks are on a tear.

Shares in Singapore Airlines Ltd. bounced the most in 21 years Tuesday while those in Cathay Pacific Airways Ltd. were up the most since 2008 after Singapore and Hong Kong declared the kickoff of a movement bubble beginning Nov. 22. Information on effective preliminaries of a Pfizer Inc. also, BioNTech SE Covid antibody pushed the Bloomberg World Airlines Index up 9.7% Monday fully expecting an ebbing tide of pandemic.

The rangers better come rapidly. At the present time, a large part of the business is running low on proportions.

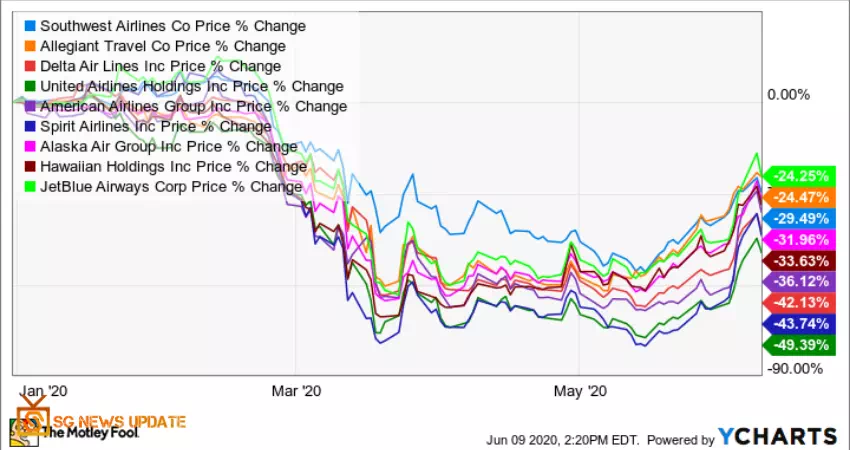

With traffic down 73% from a year sooner in September — and global flights running at only 12% of their levels a year prior — the standard way for organizations to get money by squeezing out an edge on their income is as yet obstructed. That could remain the case well into one year from now, given the feasible bottlenecks to creating and appropriating antibodies in amounts adequate to resume worldwide travel.

With traffic down 73% from a year earlier in September and international flights running at just 12% of their levels.

Usual path for airlines to bring in cash is still blocked.

- All the new obligation and value sold by the world's carriers this year adds up to almost 66% of the $241 billion.

All things considered, there's more than one approach to provision your Army. On the off chance that you can't sell boarding passes, you can in any case have a go at all that else that is not made certain about. The principal thing organizations attempt to sell in an emergency are pieces of paper. Airlines have given $88 billion in bonds so far in 2020, the greater part of the $153 billion that the business sold over the past forty years set up, as per information. Toss in the estimation of credits taken out and aircrafts' all out obligation is up by $124 billion since the finish of February, the information show. It's a comparable picture on the value side.

Japan Airlines Co. a week ago declared designs to raise as much as $1.6 billion by giving offers identical to about 33% of the current register. Singapore Airlines' $6.5 billion rights issue in June speaks to the greatest raising of extra value by any aircraft ever. The $27 billion in new offers gave by the business overall this year is identical to all the money raised through that course over the past six years set up.

In total, all the new obligation and value sold by the world's carriers this year adds up to almost 66% of the $241 billion that the International Air Transport Association anticipates that the business should gather in traveler income through the entire year.

Organizations that own armadas of high-esteem transport gear have different approaches to get money, as well. EasyJet Plc raised $170 million this month from the deal and leaseback of 11 of its planes to aircraft renting organizations. Air Canada a month ago took in $365 million from a comparable move and Wizz Air Holdings Plc and United Airlines Holding Inc. have done likewise. The gathering pledges exertion has been titanic. Think about the income of a portion of the world's biggest aircrafts in the latest quarter with their sources of income from money and contributing, short the capital consumption that carriers typically need to submit well ahead of time.

Normally airlines should see money outpourings from account and contributing counterbalance with an inflow from working exercises. That is the thing that you have with Chinese transporters, which have gotten back to some similarity to ordinariness as of late with the concealment of Covid-19. Somewhere else on the planet, notwithstanding, working the asset report has regularly been acquiring more cash than selling transport services.

You may view that adaptability as a confident sign — yet as we've contended, a hopeless second from last quarter is probably going to prompt a dismal winter for airlines. Odds are there's undeniably more to come regarding liquidations and rebuilding. Getting the business free from its Covid-initiated obligation burden could take the best portion of 10 years.

Moreover, while interest for tickets from air travelers is pretty much a limitless asset, there are just countless resources that a carrier can sell and rent back before it runs out. The blow out of bond and stock issuance this year is additionally liable to be prompting pointedly lessening cravings among leasers and investors. Despite the drop in share costs, financial specialists actually show an astounding measure of energy for carriers. On the off chance that lone travelers felt a similar way.

Coming Soon...!

Comments (0)